Special thanks to FL Research team @0xPhillan for his support.

In 2021, the total transaction volume of blockchain games exceeded $44.7 billion, the number of independent active wallets surpassed that of DeFi, and total financing of the industry was close to $4 billion. Traditional game developers such as Ubisoft and Zynga, and venture capital funds such as Bitkraft have also announced their entrance into GameFi. On the other hand, with breakthroughs in technologies such as blockchain, 5G, Artificial Intelligence (AI), Virtual Reality (VR) and Augmented Reality (AR), as well as successive entries of large technology companies such as Google, Apple, and Microsoft, people are looking forward to the prototype of the metaverse. According to Precedence Research, the global metaverse market size is projected to be worth around $1,607 billion by 2030, expanding at a compound annual growth rate (CAGR) of 50.74% from 2022 to 2030.

1. GameFi combines games with crypto economic incentives

In general, GameFi should be "Game + Crypto", a product that combines games with financial properties of DeFi. The emergence of GameFi upgrades the behavior of "playing games" to a "labor production" besides merely a consumption process. We are optimistic about GameFi in the long term due to its potential of endowing game assets with certain value in the physical world as well as the metaverse.

Venture Capitals' high expectations and people’s curiosity about the metaverse have led to a continued popularity of the GameFi market. Regarding how the combination of various Web3 elements such as NFT, DeFi, and token economics affect the way people play games, we try to break down and explore: What exactly can Crypto bring to the Game?

1.1 How GameFi captures value

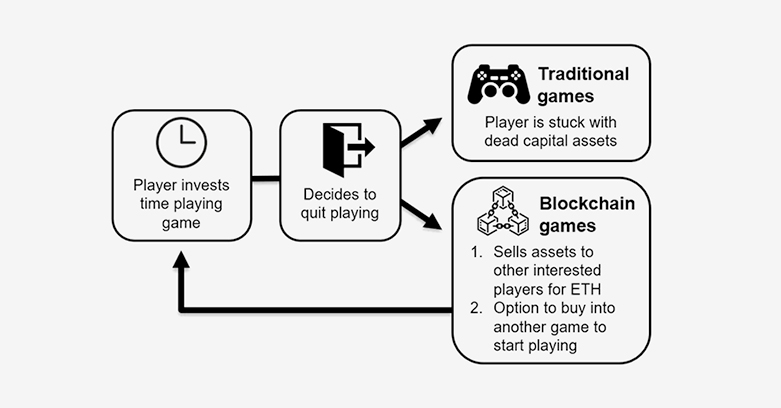

In the movie Ready Player One, game developers were blamed for dominating everything like a "God". If necessary, the game developers could directly shut down the servers and delete all data, and the time and money invested by players would no longer exist.

From the perspective of content production and consumption, playing games is merely content consumption behavior. The value of virtual assets (game points, hero level or skin, pets, etc.) and labor (spending time and money) are not recognized in the physical world. Moreover, development teams have the absolute right to monopolize the games as they wish. If teams go bankrupt or shut down servers, the output and income of players will cease to exist.

Which part of the game needs to be on-chain and how can we balance the on-chain and off-chain parts? Looking at the difference between Web2 and Web3, the introduction of blockchain guarantees the ownership and traceability of digital assets, which in turn brings about changes in production relations. We think that in the short term, transaction materials used in blockchain games such as tokens and NFT, should be prioritized to be put on-chain. Full-on-blockchain games have not yet appeared due to current limitations of blockchain technology such as high gas fee and low transaction speed. Let’s discuss the way blockchain and games are combined from the perspective of productivity and production relations.

"NFTization" of production materials

In traditional games, the production materials of players are generally bound to their personal accounts. The labor (time and money) paid by the players contribute to in-game economic systems. Digital assets between accounts of different games cannot be traded.

The uniqueness and immutability of NFTs are the key to solving the problem of game asset ownership confirmation. In the foreseeable future, players will also be able to mortgage, lend or loan their game items, analogous to the financial market. For example, the blockchain game Otherside Meta sold 200k NFTs, with multiple elements related to potential rewards and game productivity, to build a highly imaginative metaverse world. Owning an Otherdeed (its token), or access to digital land, is more like owning a simulated farm. Land owners see their unique artifacts and potential resources, and will be part of the upcoming metaverse with special events, tests and builds.

"Tokenization" of Game Financing and Earnings

The introduction of tokens allows financial outflows into and out from a game. On the one hand, tokens can undertake the transaction function of its in-game resources, facilitate players to sell, lease, mortgage their game assets as a liquidity provider (LP) as well as improving the profitability of game investors. Take Axie Infinity, which was a big hit since 2021, as an example. Players can get token SLP and game Axie elf as rewards through games, which is equivalent to replacing “liquidity mining” in DeFi with “playing games and mining” in GameFi.

On the other hand, tokens can improve the financial liquidity required by games from development to distribution, removing intermediaries to reduce costs. For example, independent developers like Star Atlas studios can raise funds, either through NFT sales before the game is released, or publishing tokens to investors, similar to the old-fashioned way of selling equity.

"DAOization" of GameFi Developer Ecology & User Community

Ashley Black, Head of Google Gaming APP, once said, "Developers staying active in the gaming community can help increase user engagement inside and outside the game, and help build the credibility of the game brand." How to encourage more real users to join GameFi, convert more non-content creators into content creators, those are all pain points in traditional games. With the maturity and abundance of Web3 infrastructures such as DAO methodology and management tools, the application of DAO in GameFi is also a direction we are optimistic about. The prosperity of the developer ecosystem, the transformation, growth and retention of real players are all our concerns.

To sum up, the significance of involving crypto into the game is:

1 Quantitatively capturing productivity: Players in the virtual world can experience a similar process of content production, investment and consumption in the real world. The output of virtual world labor, number of players, time spent and gaming ability are reflections of productivity which can be tracked on-chain.

2 Change of the production relationship: The rights and obligations of players and other organizations (other players, game developers, guilds, etc.) are fairly defined, that is, the game players are owners of virtual assets instead of merely being players.

1.2 What is the relationship between blockchain games and traditional games?

By the end of 2021, there are about 49% (~1.4 million) of independent active wallets in the industry are connected to GameFi, driving GameFi related NFT transaction to $4.5 billion. Although the blockchain games industry is highly active, the transaction volume is small at present. Measured by revenue, the NFT market of GameFi is significantly smaller than the market of traditional games and IP content ($173 billion). According to Sensor Tower 2021 report, mobile games occupied more than half of the market revenue, while that of GameFi is less than 3%. GameFi players only account for a small proportion (millions players until October 2021 according to DappRadar statistics) of the 3 billion gamers in the world. Thus, there is not much overlap between gamers and blockchain users, many players have not yet entered the market.

We don’t assume that console, PC, and mobile games are rivals. What matters is the content, not the container. Although games and other entertainment apps such as TikTok competing for users limited attention, they are targeted different audiences to some extent. New generation needs are continuously emerging so in the long term users attention market is large enough for competition. Traditional big game developers have competitive advantages of industrialized production of game content, while the native web3 game developers can also be the pioneer of innovative modes. Thus, we don't think blockchain games and traditional games are in a head-to-head competition.

Instead of asking whether or not GameFi will replace traditional games, would it be possible that they compliment each other? There is an opportunity here to attract both Web2 and Web3 users. We are looking for answers to questions, such as:

- Is it still necessary for traditional game developers to take the lead in self-reform in the field of Web 3.0 games? Or will Web 3.0 cultivate its native game companies?

- In the next cycle, will game-native tokens go mainstream in the market? Will Web3.0, NFT, and token-driven communities create new game types?

1.3 How can we determine the long-term potential of GameFi?

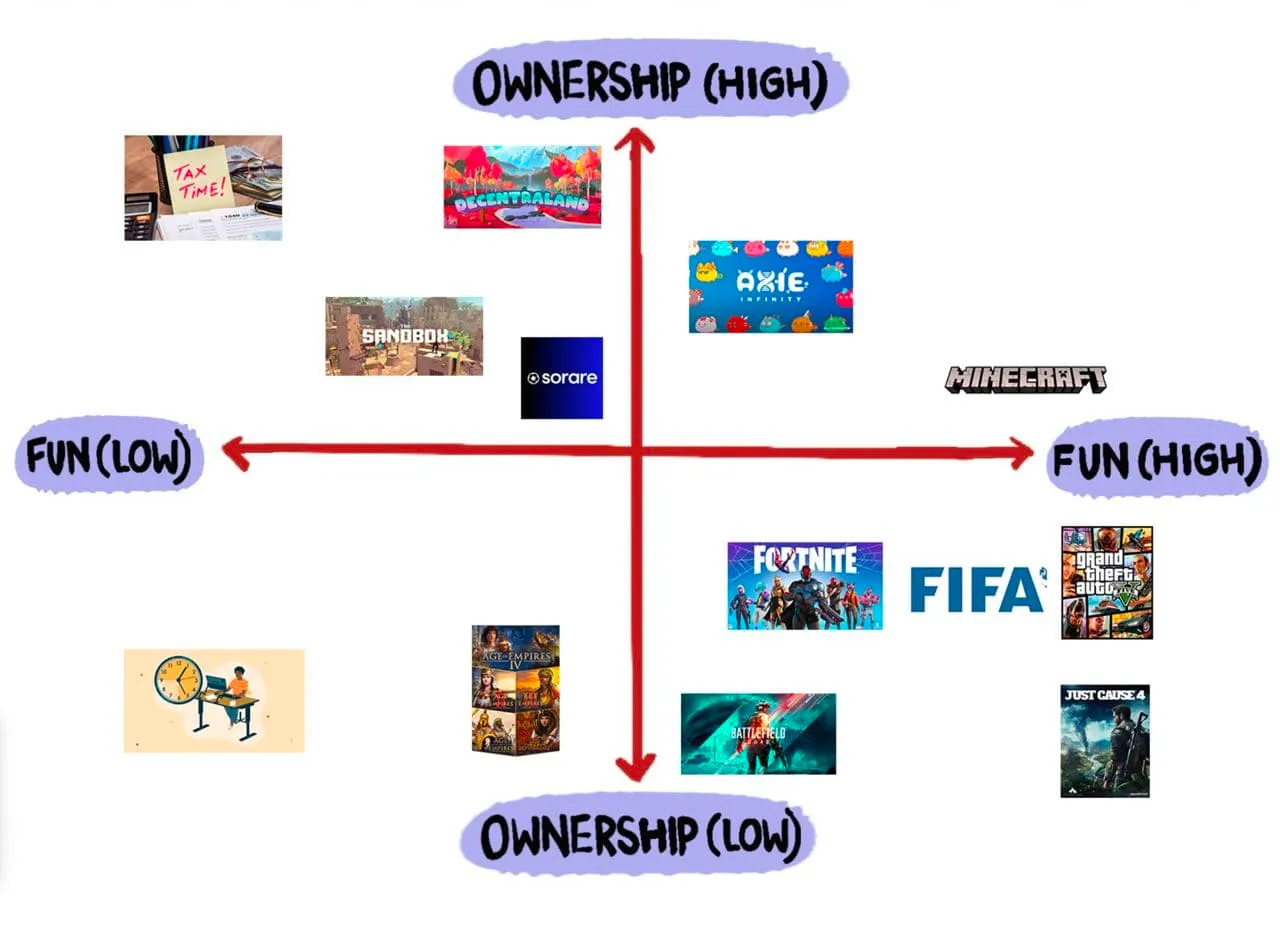

Nowadays, many GameFi white papers try to demonstrate their potential value directly by benchmarking traditional game market conditions. However, from a dialectical point of view, not all types of games are suitable to be on-chain, which leads us to our concerns - what types of games are suitable for on-chain modification at this time? In what new aspect can native Web3 games capture opportunities? Here we try to propose some new framework and perspectives.

x-y coordinate: strong ownership and high interest

In this coordinate system, the lower left corner corresponds to work in real life, as the default game (low ownership and low interest) we ourselves are always participating in. The upper right corner corresponds to our vision for the metaverse: strong ownership and fun.

y-z coordinate:

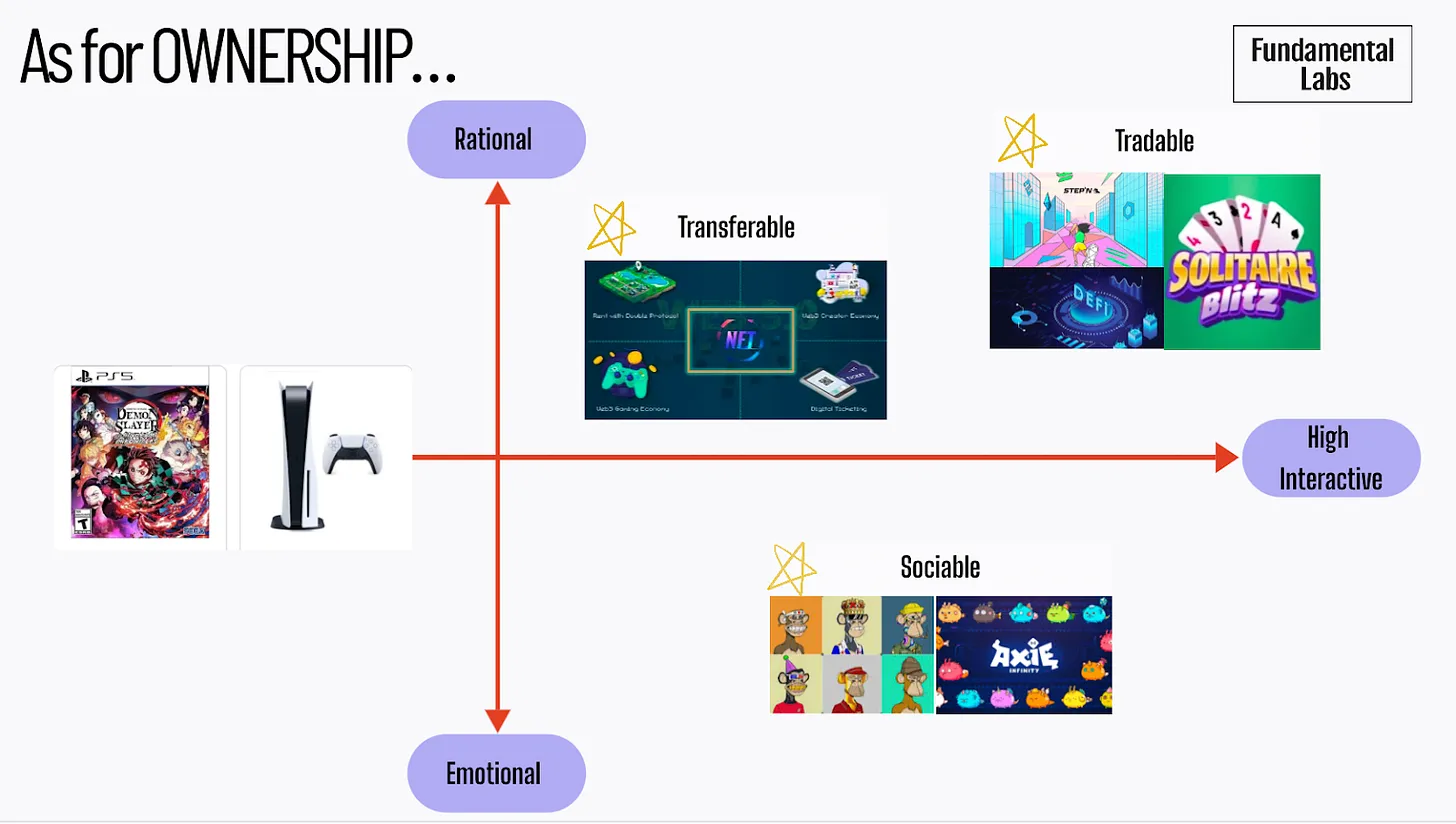

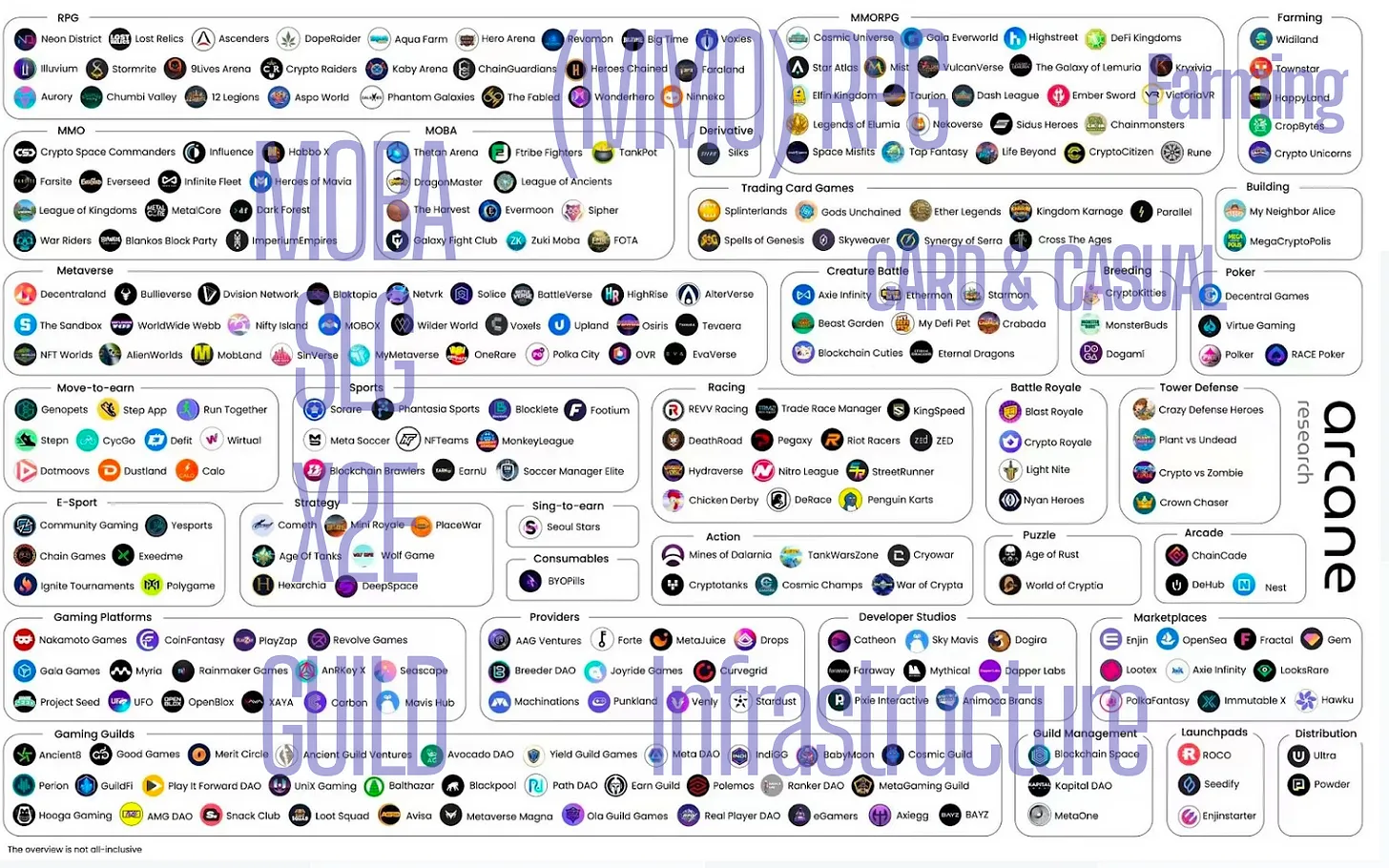

Traditional games are categorized by genre with similar gaming experience. With the development of the times, there are more subdivision types. Just as it is no longer enough to classify movies only by horror or action ones, it is not accurate enough to determine what games are suitable for on-chain modification merely by RPG (Role-playing game), ACT (Action Game) and other genres. Here we provide a new framework based on “ownership” from interactive trading perspective and “fun” from game design perspective.

1.Transferable

As early as the 2000s, game items trading markets have emerged in the "Free-to-Play" era, especially in various online games. Some studios sell high-level props or accounts to other players by paying money, and even provide services such as cheating plug-in scripts. This kind of studio once was disgusted by developers and players because it will cause unfair game order.

The application of NFT is a good starting point for the ownership and management of virtual assets. Considering similarities between skin items and NFTs. Skin items in game, which offer buyers no added competitive advantages other than cosmetic appeals, are in high demand of transaction from enthusiastic fans. Game studio Riot Games has become a multi-billion dollar company by selling skins for its hit game League of Legends.

2. Tradable

In September 2021, Andre Chronje, founder of Yearn Finance, tweeted that the future DeFi trading model may turn out to be more gamified. The development of GameFi is also fulfilling Andre's point of view. For example, Alien worlds and Farmers world, which are often listed on the TOP10 GameFi list, are essentially DeFi products wearing the coat of games. Stepn also relies on ponzinomics to continuously attract new speculators.

Different from the transferable property, "tradable" emphasizes the financial characteristics. It might bring asset risks and speculative behaviors, which will lead to the decline of game quality and negative user experience. Looking forward to the long-term and healthy development of the GameFi industry, "Game + DeFi" products only account for a certain part. GameFi cannot only rely on attracting crypto users. Though speculation can be a legitimate part of games, creating meaningful game experiences will be key for GameFi to go to the market.

3. Sociable

Although many single-player games with weak interaction also have a large number of loyal audiences, we think that GameFi should have a certain degree of social property, which is positively related to the above-mentioned tradable or transferrable properties.

Just like projects such as Otherside Metaverseintegrated with ApeCoin in order to attract users from the BAYC and surrounding NFT ecosystems,immutable property ownership in the game can incentivize players to build stronger community relationships in guilds or communities. Game creators can ultimately gain some value from the ecosystem and have more incentives to create high quality content.

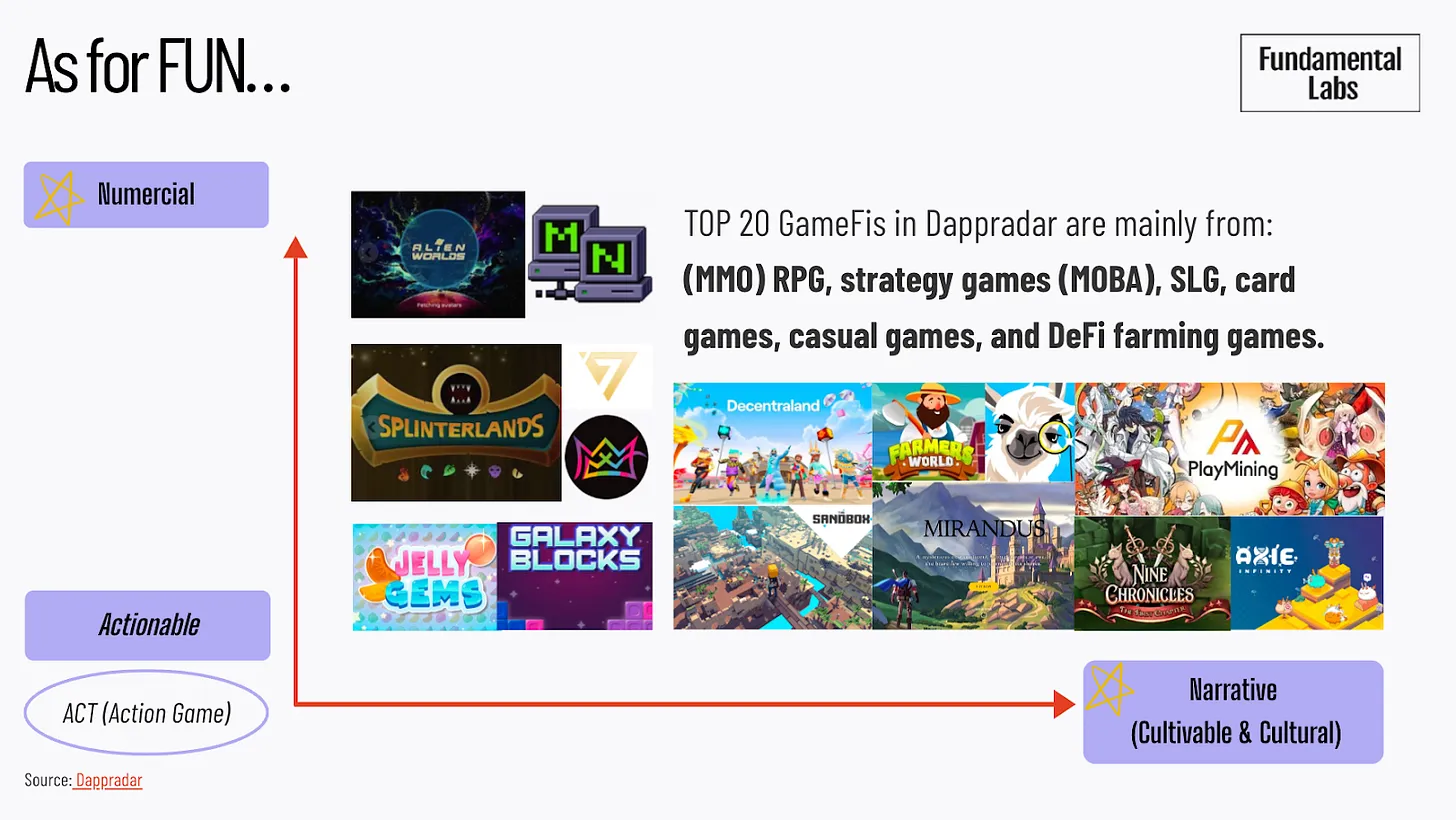

According to where games attract players, we try to propose another framework centered on user experience, unlike traditional methods centered on game mode. We define another three properties: narrative (whether accumulation-based & cultural), numerical, and actionable. In fact, most popular games are a combination of above properties, probably the focus is different.

- Most games that focus on narrative property have complete world views and values. Often gameplay (such as playing roles in MMORPG, experiencing plots in simulation games), and art performance are the expression of core storylines. We split narrative property into "accumulation-based'' (refer to cultivable in the picture) and "cultural".

- The so-called "numerical" refers to the mathematical settings and economy working in the game system. A good numerical design needs to balance various challenges corresponding to different stages of user groups. An important role of numerical property is to quantify the perceptual world in the game. For example, how many gold coins a player should have, how much HP a character should have, and how much damage a certain skill can hurt the enemy, those are intuitively displayed to players in the form of data. By contrast, in most games the speed of running and the attack range of a certain skill are experienced through operations.

- Games that focus on actionable property often train players’ reflexes, hand-eye coordination, and reaction time. Think classics like Pitfall, and other switch games that involve a lot of virtual running and jumping. The plots of those games such as Super Mario are relatively simple. High-level action games have already had a high threshold for development and operations. Many independent game studios can only introduce cultural elements or other art design elements to establish a differentiated competitive advantage.

4. Numerical

If rule design can be considered as muscles and art performance can be considered as skin, numerical design actually connects all of them, which encourages players computing optimal game strategies through analyzing. Users allocate resources, and numerical designers predict corresponding numerical curves to counter them.

Game players who prefer numerical gameplay are generally more "utilitarian" than that of other game types due to result-oriented rules. They have particularly strong feedback on the game rules, attach importance to personal accumulation of experience, and are willing to calculate return rate in order to figure out optimal strategy. From this, we believe that the explicitness of numerical design is a cut-in perspective for evaluating chain modification games. This is also a reasonable proof that initial GameFi is mainly adapted from (MMO)RPG such as CryptoKitties, and strategy games.

5. Accumulation-based (Cultivable)

Many open-world gameplay or games with accumulation-based systems have relatively long user retention (even being able to build up an intellectual property (IP), such as Genshin Impact), one of the key points is to provide enough emotions or feelings for users. Final Fantasy 14 is an example of an online MMORPG in which players can purchase and raise pets, where spending of money can help the cultivated progress faster. Even if players cannot earn money, they are willing to spend a lot of time or money to accumulate their own assets. Another key point might be the "emotion sunk cost", like players might produce emotional dependence on cultivating or parenting virtual pets. Narrative driven single player games such as Red Dead Redemption 2 or Fallout 4 allow pets (horses, dogs) to travel with players, the focus is to experience the narrative plots.

6. Cultural

Audience groups with similar world views and values will quickly condense and develop into a culture, which will continue to progress, develop and inherit. There is a chance that GameFi can attract attention by using external resources to improve the loyalty and willingness of internal players to pay. Publishing of IP-derived films, literary works and peripheral products are potential construction materials.

The cutting-edge projects have come out of the circle with their unique IP or cultural design concepts and excellent product capabilities. For example, DEP, which is a chain created by Digital Entertainment Asset Pt. Ltd. (DEA), focuses on distinctly Japanese style GameFi and NFTs. Although new, both DEP and its GameFi PlayMining have relatively good data performance. Active users exceeded 22,000 until 2022, April 13, which is already close to the level of DeFi Kingdoms.

2. GameFi Status Quo: DeFi is the core and games are only the skin.

First, let us review the development history, key driving factors and problems in each era.

2.1 The development history of GameFi

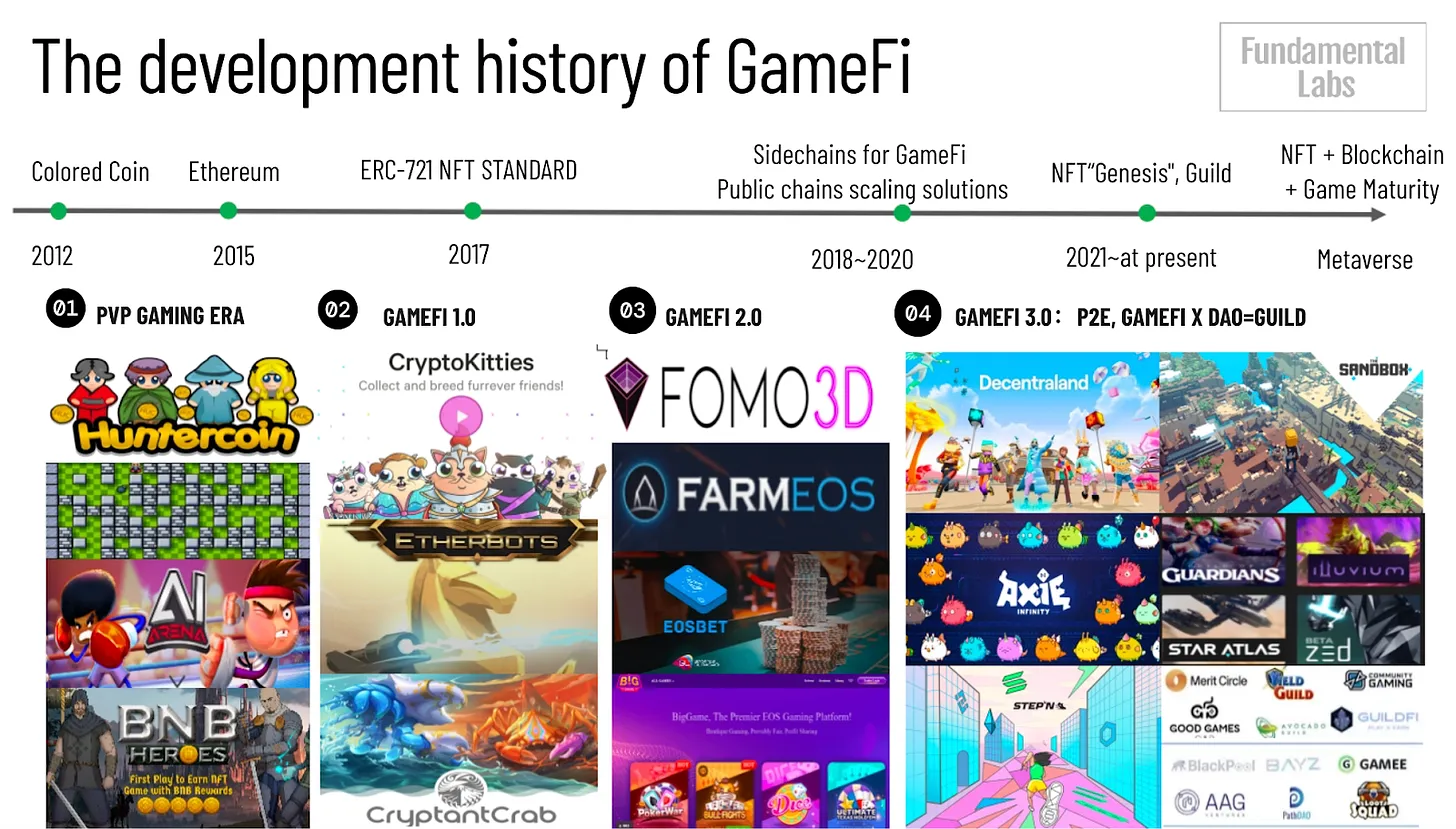

Player-vs.-Player (PvP) Gaming Era:before 2017

In fact, since the beginning of Bitcoin, there have been pioneers who have made much efforts to involve blockchain into online games. For example, in 2013 the popular player-versus-player (PvP) games such as Gambit (offering board and card games for gambling), Bombermine (the blockchain Bubble Hall), and Minecraft (traditional game), which allow players to monetize games, similar to the earliest attempt in the field of GameFi. Soon, experimental programs like Huntercoin began to use blockchain technology (without issuing tokens) to encourage farming. It was also considered as a successful practice in Web3 community operations.

Most blockchain games in this period were tedious. The only purpose for playing games was to make money. The main advantages of the business model are low cost and high initial profitability. After 2015, the emergence of Ethereum opened up new possibilities for game developers. In addition, high-level programming languages such as Solidity have enabled smart contracts to flourish and the emergence of ERC-721 standard non-fungible tokens (NFTs) has stimulated tremendous innovation in the GameFi industry.

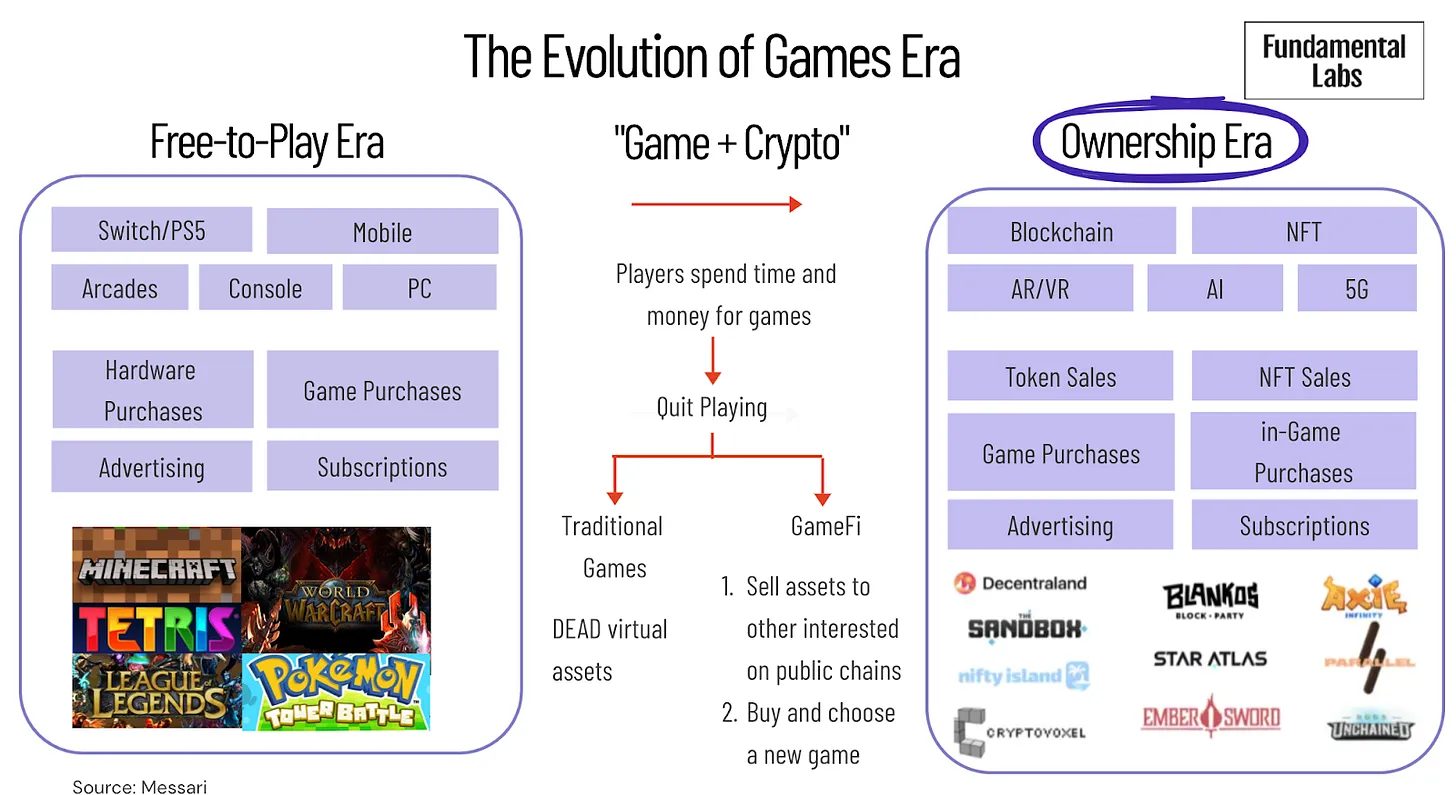

GameFi 1.0:after the end of 2017

The history of GameFi starting from "CryptoKitties" in December 2017. At this time, GameFi had almost no token economic system, but NFTs have been applied. The gameplay has simple cultivable systems, though the overall life cycle of games is short.

However, the limitations of blockchain have affected the continuous user growth of GameFi. The crowded network and high transaction fees of Ethereum have reduced their enthusiasm and raised the entry barriers for players. The daily activity users (DAU) of CryptoKitties once reached 15,000, but it dropped to the level of 1,000 in just one month, and the transaction volume had shrunk seriously.

GameFi 2.0:2018 - 2020

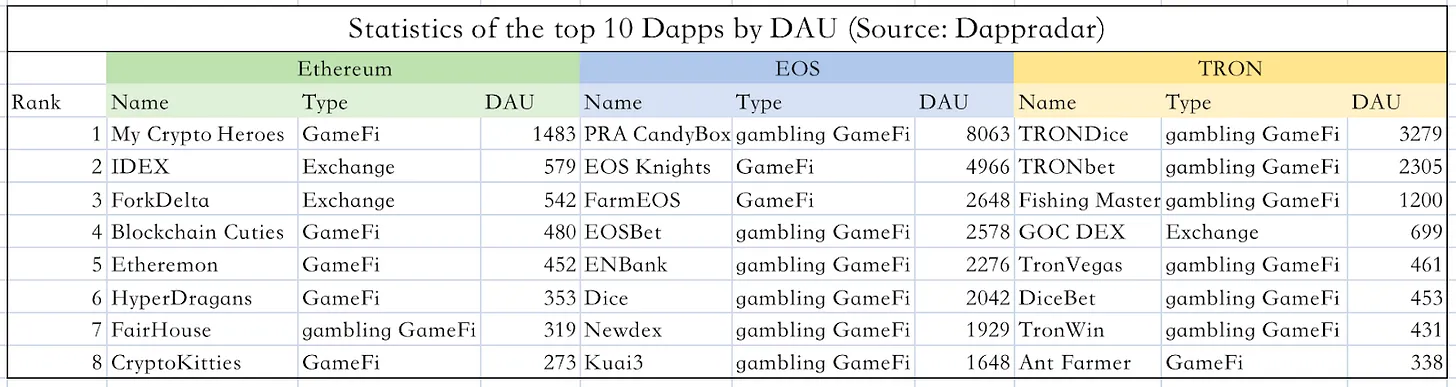

Beginning in the 2018 H2, more speculative gaming DApps represented by Fomo3D (EOS Dapps: Here’s a List of 10 Popular Dapps in 2019)supported the “prosperity” of GameFi 2.0 period. According to the statistics of "2018-2019 Cryptocurrency Market Annual Report", until December 31, 2018, there were about 1,609 DApps in main public chains. Among them, the gambling category was in the top two, accounting for 29% respectively.

At this time most players in GameFi are driven by profits, and the user retention was far shorter than that of other DApps. Once a certain gambling DApp is found to be unprofitable, players will go away. That leads to a short life cycle of farming blockchain games, which last about a week on average. Due to low development barriers and "short-term" profits, the influx of hackers had caused a huge threat to the security of smart contracts in GameFi. Several game platforms such as EOSCast and EOSDice were attacked by hackers frequently, whose total loss had reached 395,000 EOS and 13,000 ETH (exceeding $27 million) at that time (until December 2018).

A large number of players were still outside the GameFi market due to frequent security problems and scarce high-quality game contents. In 2020, the market showed much interest on game development platforms and tools. Some public chain platforms and traditional game development teams entered the market one after another.

GameFi 3.0:start from 2021

Until 2021, the NFT transaction market has generated more than $23 billion, whose commercial value has been widely recognized. Starting from the well-known game Axie Infinity, GameFi 3.0 is in the stage of widespread adoption of NFTs and token issuance. Guilds also appear in the ecosystem as the role of integration and distribution. Many blockchain games span multiple chains and have mixed game types to enrich the gameplay and improve experience.

The rental NFT protocol – Double Protocol also launched a new NFT standard ERC-4907 on June 30, 2022. According to the original discussion of the Ethereum Developer Forum, NFTs will have application scenarios where the user and the owner are not the same person. For example, some investors buy some practical NFTs such as virtual land, and they may hire others for construction. The separation of NFT rights and ownership has been clarified. With the improvement of Web3 infrastructure and users acknowledged through P2E blockchain games, we are looking forward to the entry and performance of experienced game development teams or studios.

2.2 Is "Play-to-Earn" a viable long-term solution to GameFi?

Since it was reported that Axie Infinity made a revenue of $334 million in just 30 days in Aug 2021, the entire Web3 has noticed Play-to-Earn (P2E). The attitudes are very polarized, some see it as a must-have gameplay of blockchain games; others see it as a Ponzi scheme in the name of games. The indisputable fact is that more and more companies and startups are trying to launch P2E blockchain games. We are curious about the status quo:Why is Play-to-Earn so popular? Is it a viable long-term solution to GameFi?

Let's first figure out what problems P2E has solved.

The implementation of Apple's IDFA policy and the bottleneck of Internet users growth show that - new users are more and more difficult to acquire, and the cost of user acquisition and retention is rising. How to attract new users and improve retention at a low cost has become a headache for many startups in the traditional game industry.

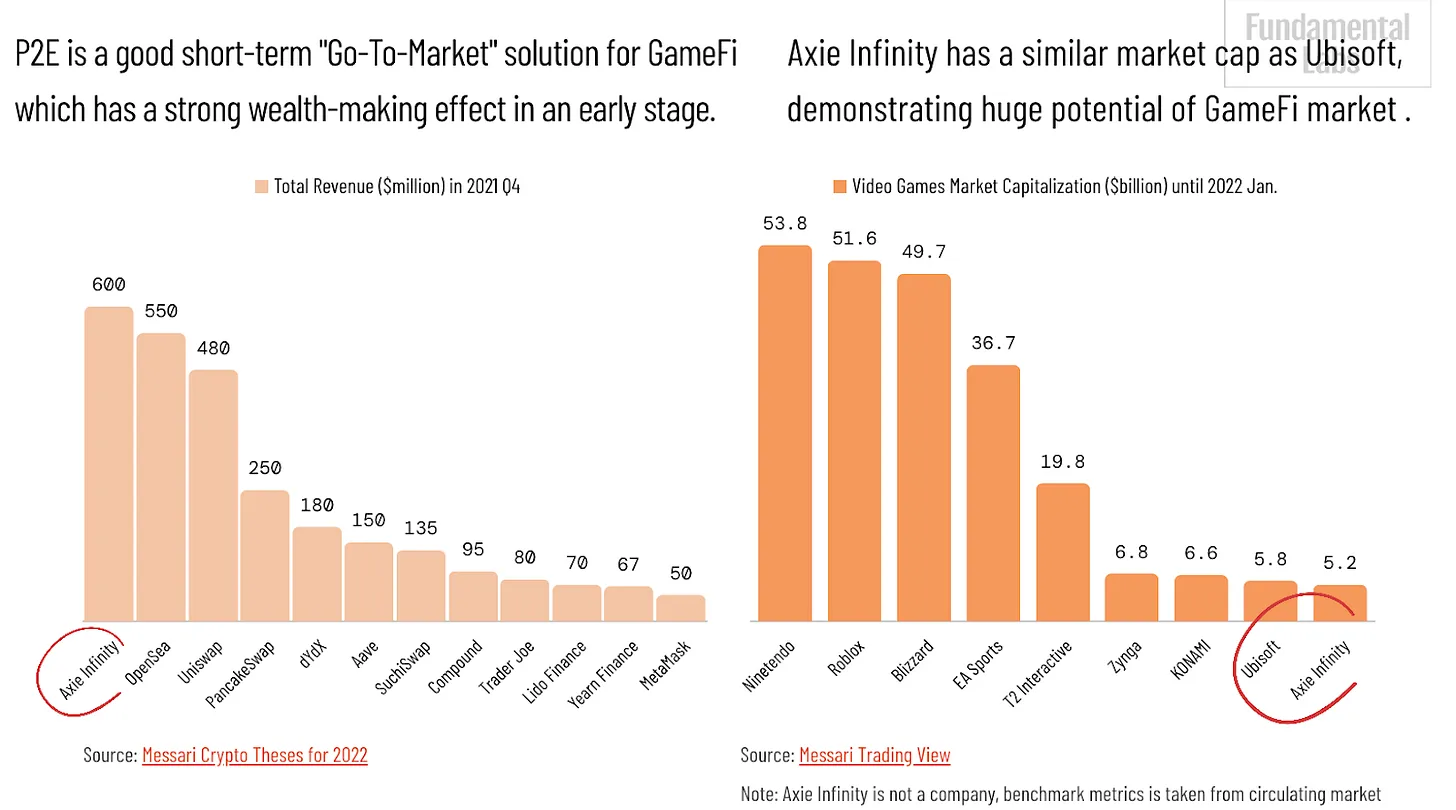

P2E provides strong liquidity for GameFi from development to distribution. Compared with Roblox taking 17 years to reach $100 million in monthly revenue, Axie Infinity made a revenue of $334 million in just 30 days in Aug 2021. P2E is a good short-term "go-to-market" solution for GameFi which has a strong wealth-making effect in an early stage.

2.3 What problems might P2E bring up?

1 Gresham's Law: "Bad money drives out good money"?

There are examples in Web2 similar to "Play to Earn", many mobile games such as racing video game Asphalt invites players to watch ads so that they can get more coins or energy to play in a new round. User growth benefited from those marketing ways in the early stage, but they had almost the same dilemma in the end – "how to improve the user retention and quality".

The premise of the P2E business model is that there are enough new people entering the market, and the token distribution model can be designed sophisticated enough to extend the life cycle of the blockchain games. However, it does not solve the long-term lack of playability problem. P2E might attract speculators quickly becoming the first users. They occupy a lot of valuable NFT resources but might not actively contribute to the game ecosystem, and may even disrupt the order due to vicious competition for benefits.

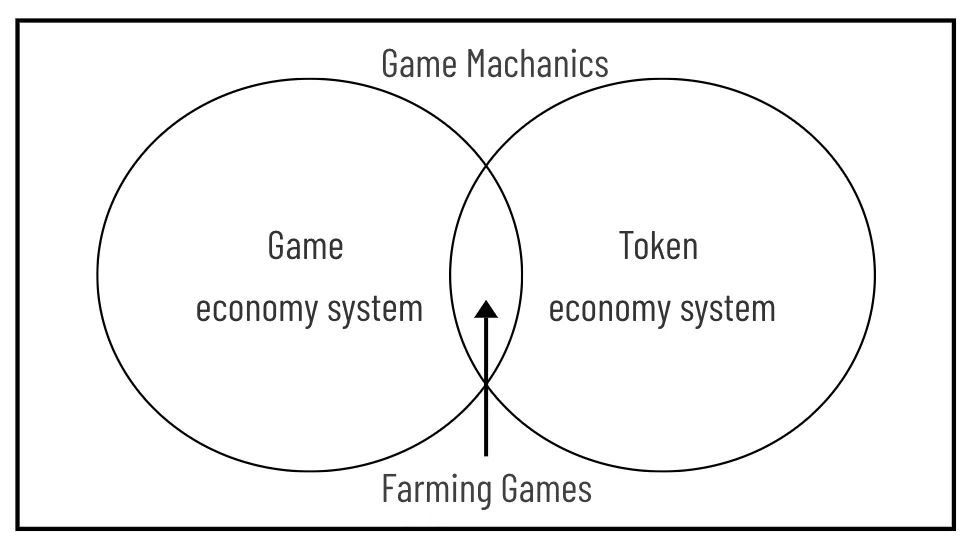

2 Game economic system versus Token economic model?

The quality of the economic system may not be the most important factor in the early stage, what is important may be some independent elements in the structure of the economic system, such as gameplay, art performance, and so on. But if a game hopes to operate well in the long run, its economic system must work well.

Although both are part of the game rules, the token economic model (where miners provide service in exchange for a cryptocurrency and users consume service) should not be confused with the economic system (the production and recycling of built-in game resources). Many blockchain games focus on designing a complicated or a certain speculative token economic system instead of creating an entertainment-based product with balanced economy, which "puts the cart before the horse".

The blockchain game should not be purely financial arbitrage. If the gameplay of a blockchain game simply relies on the Ponzi scheme like X to earn — absorbing money from new users by setting a high entry threshold and distributing rewards to old users. If players continue to lose, blockchain games will only face the problem of how fast or slow the death spiral is.

2.4 GameFi should focus on good products experience more than sophisticated token economic models

To some extent, it is undeniable that the fact that Axie Infinity's revenue surpasses that of King Glory, shows that users who aim to earn have the potential to create great value. We consider that the current market exaggerates the advantages of P2E. "Paying players forever" can be a gimmick – an efficient short-term way of Go-To-Market, but it's clearly unsustainable. GameFi should at least ensure users experience like traditional games in order to attract players who are devoted to the game itself.

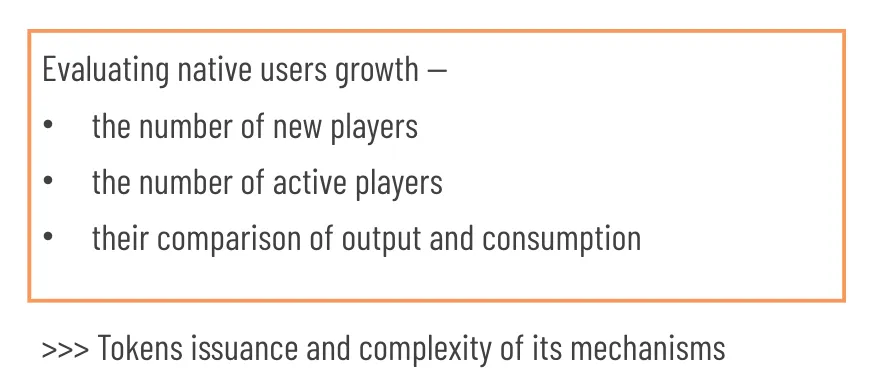

We tend to focus on evaluating the growth of native players, rather than the issuance of tokens or the complexity of its mechanism (a framework for evaluating token economic models) in the early stage.Especially if a blockchain game chooses to issue a token, why should people hold it? How to attract more and more real investors, and users, and let the digital assets in the game field have real value should be a key question to answer. We expect that in the test of bear market, blockchain game developers’ path might be more clear: income-driven games with a gig economy model or fun-driven games with token economics.

3. Problems need to be solved for long-term development of GameFi

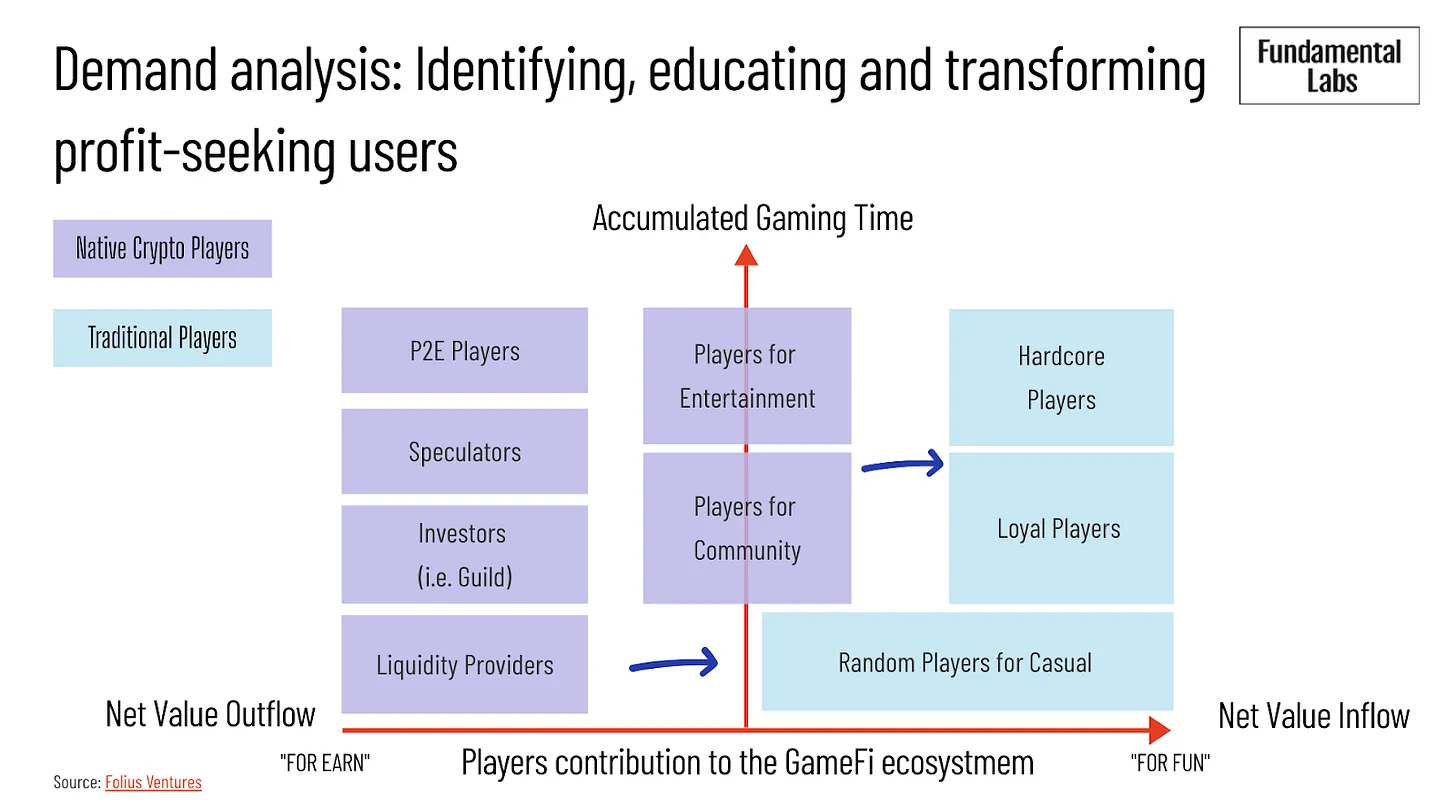

3.1 Demand analysis: How to attract real players who have not entered Web3.0?

Starting from the motivation of playing games, we make a rough division of players: one type of players is "social or cultural identity-oriented", and their core requirement is based on the identity of certain values in the game world or social interaction with others; the other type is "self-experience first-oriented", who pays more attention to what kind of experience the game brings to them (goal achievement and entertainment experience).

Those two needs of game players are either more or less, but the current play-to-earn model of GameFi does not focus on the needs and pain points of traditional game users, but attracts a large number of "return on investment oriented" players. Moreover, such players do not overlap much with ordinary game players, and are even rejected by some hardcore players (Why Gamers Shouldn't Hate NFTs) .

Realizing the capital outflow risk caused by the seeking-profit inertia of native crypto users, one way of thinking is guiding them to become blockchain games value contributors through constructing such as community, identity and playability. Value inflows such as encouraging players consumption and investment through emotional driven factors, which is also a fair value exchange between games and players. We have observed that many startups are currently building "bridges" attracting users from Web2 to Web3, innovating in publishing and distributing channels.

3.2 Supply analysis: How to cultivate or discover elites who are both good at game design and blockchain?

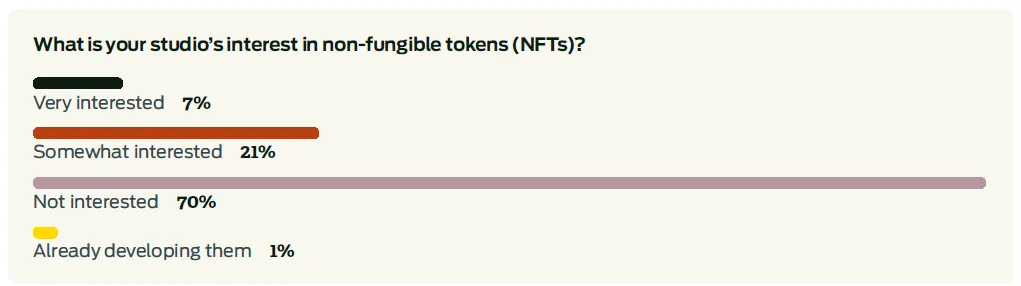

The 2022 Game Developers Conference report surveyed more than 2,700 game developers and found that the majority of gaming industry professionals are not interested in crypto currencies (72%) or NFTs (70%) at all.

How to empower developers and form a healthy and lasting creator economy is a question that needs to be answered patiently. We see that the supply-side opportunity is that platforms and engines like Enjin, Ultra, Forte, MixMarvel are needed to empower traditional game developers, help them understand blockchain technology, and understand the GameFi architecture and rules of Web3 .

3.3 Where will GameFi go in the near future?

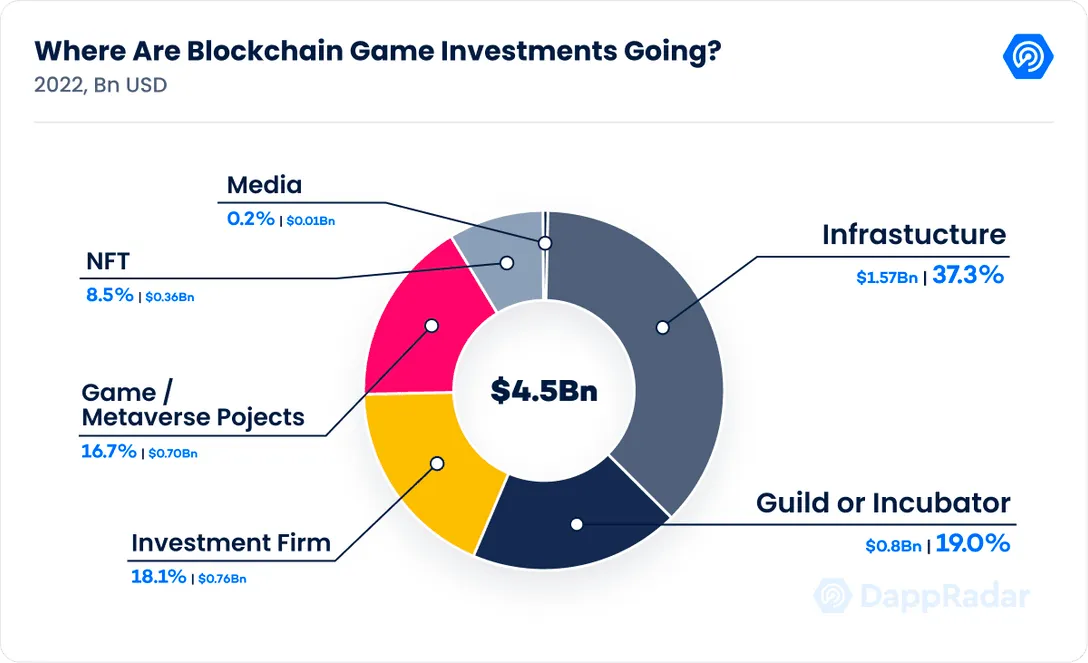

According to the DappRadar Games Report in May, investments will probably surpass $10 billion for the year, though the bearish outlook of the crypto space might reduce the investment appetite in the short term.

There are four main roles in the game industry: developers, publishers, distributors, and users. The voice of each role changes with technological iteration and industrial restructuring. At this stage, game developers, centralized advertising monetization and user growth providers monopolize most of their interests.

Aleks Larsen, co-founder and COO of Sky Mavis (the company hatched Axie Infinity), mentioned in an open meeting in May 2021, "This is a game that is not available in any app store. By the end of 2021, we went from 36,000 people to 2.5 million people now." Further cost reductions in development and operations through the application of crypto are extremely attractive, we consider this opportunity will be preferentially captured by gaming guilds.

At present, guilds provide players with game assets to lower the entry barriers. In the future, guilds may be the key entrance to develop GameFi. Some people may have worries whether the guild will also become a centralized profit monopoly in the future. It is worth responding that, from the perspective of investment, guilds are beneficial to capture at least two layers of return: on the one hand, the beta return is from the GameFi industry, which is not affected by any certain blockchain game, as long as the industry is growing; on the other hand, the alpha return is from the potential high-quality blockchain games hatched by guilds.

However, many guilds now issue tokens from the very beginning, but most of them don't know what users should be targeted and why users should hold the tokens. We are looking forward to the vitality of users-education-oriented and service-oriented guilds, rather than that of issuing tokens simply for investment purposes.

Looking at the next layer, one opportunity that we are focusing on is the infrastructure.

Since some chains are not strong enough to support the simultaneous transmission of large-scale data, high network costs, transaction costs and slow processing time caused by financial transactions (leasing, lending, mortgage) are also problems that GameFi needs to face. In early 2022, transaction fees of a blockchain game Sunflower Farmers soared to 500 gas fees on Ethereum, which emphasized the need for low-cost alternatives. Therefore, some games have developed their own blockchains, and turning to the development of private chains is also an idea to solve the problem of in-game scalability. For example, Axie Infinity uses Ronin or Splinterlands uses Hive.

Providing developers with development tools and a suitable environment that supports cross-platform is also an essential opportunity. nteraction between different public chains and cross-chain are theoretically feasible, but cannot be realized in a short period of time. Wemix, a blockchain game represented by a South Korean game company Wemade, can lower the technical and financial thresholds of developers. By connecting with intermediate chains, the problems of low TPS (transactions per second) and excessive fees are solved.

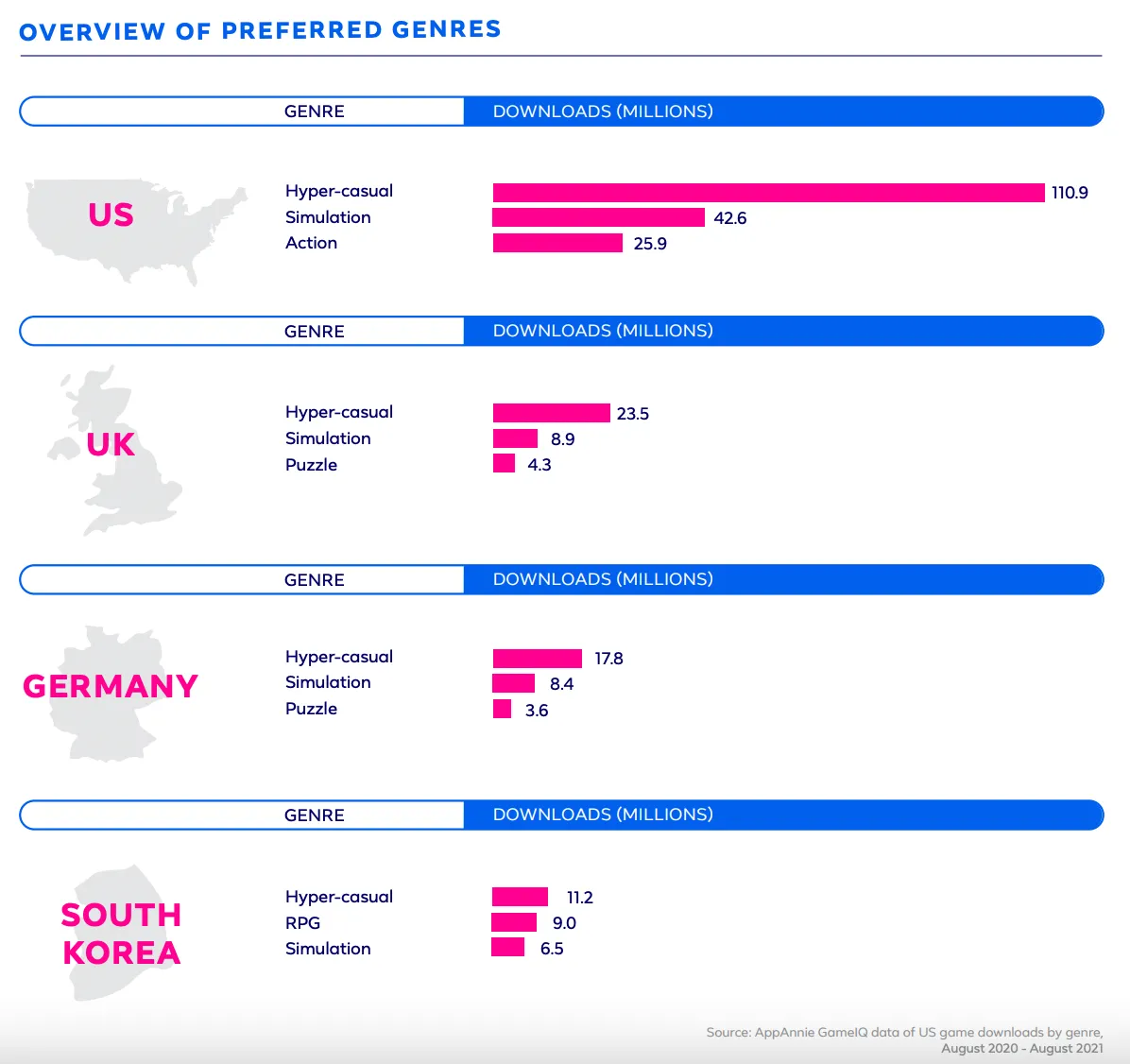

3.4 GameFi should pay attention to improving localization adaptability

The development of the game market is not only driven by the internal factors of products, but also external factors including cultural differences, accounting policies, and regulatory environments in various regions. The report Facebook Gaming in 2021 shows that although the motives for playing games are similar, there are obvious regional differences in players’ preferences for game types and consumption habits (take the four countries below as an example, new users: in March 2020 since the epidemic outbreak).

Ashley Black, Head of Google gaming apps, once said, "It's important for developers to understand these cultural and linguistic differences. Since the game is a global thing, there's no one-size-fits-all approach." For example, in the US market, the price of in-game purchases usually ends in "$0.99", while in Brazil, it is better to mark the price as an integer. Ashley Black emphasizes that even this subtle difference will affect how gamers feel about the game. We believe that a good blockchain game should pay enough attention to creating culture identity and worldview value for users are important. In addition to the playability, we also focus on the capabilities of localized operations.

4.5 Some new thoughts

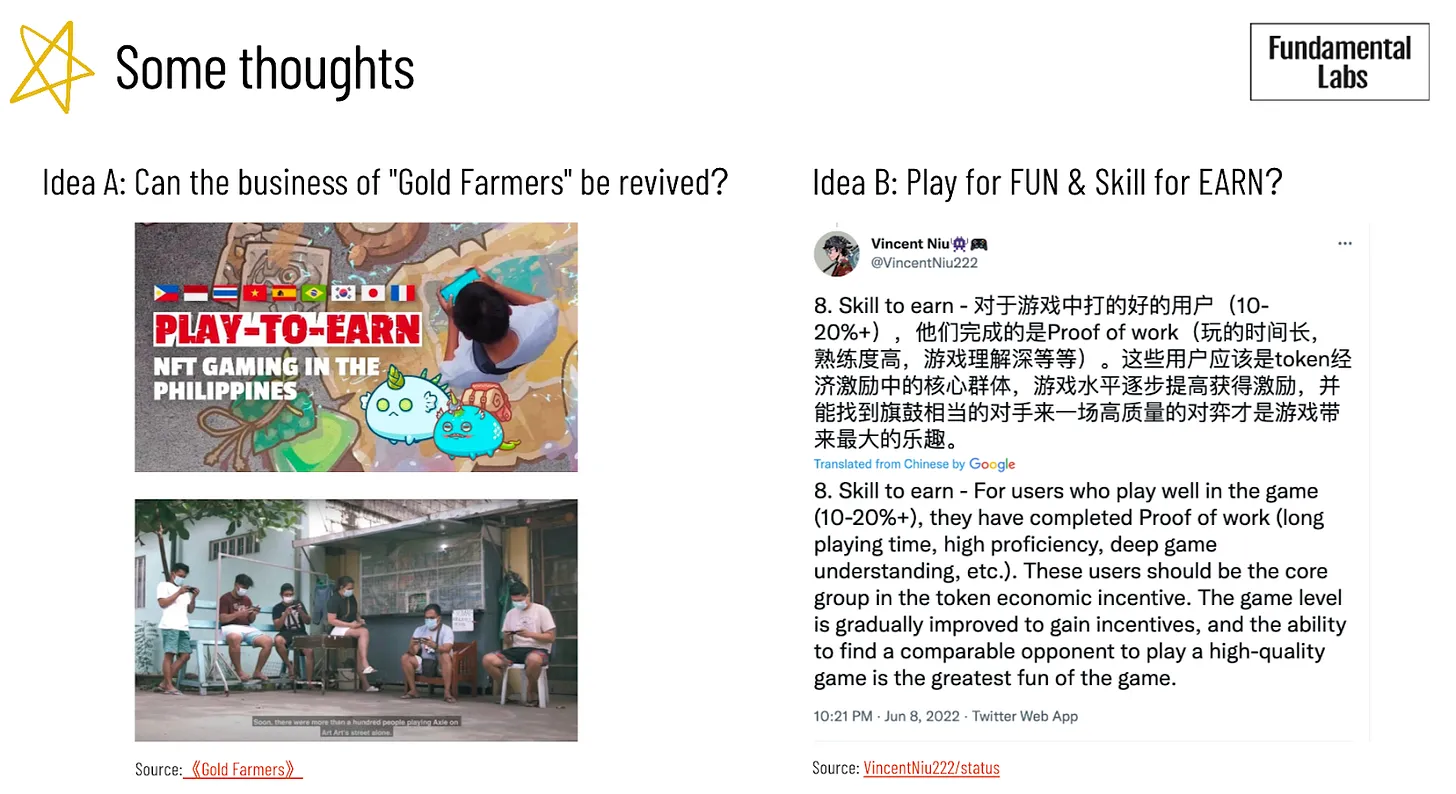

1 Is it possible to revive the era of "Gold Farming"?

In 2005, Ge Jin made a documentary about the economy of online games. At that time, ten thousands of young people in China were making a living in games such as World of Warcraft. The virtual awards and equipment they won in the game could be exchanged with dollars from foreign players. This behavior is called "Gold Farming", and these players are called "Gold Farmers".

Similar behavior can be observed in blockchain games today. Taking Axie Infinity as an example, there are already millions of people in Southeast Asia who play it as a means of making a living. The most successful guild, Yield Guild Games, has recruited more than 4,000 full-time players and issued its own token YGG.

The "Play to Earn" model of blockchain games has a common foundation with the "Golden Farmer" business 15 years ago, which is the "difference in time value". Axie and YGG can rely on low-income countries such as the Philippines. Because the demand side has a large number of high-income people who would rather spend money than spend time to acquire virtual assets in the game, while the supply side has a large number of labor who are willing to spend time playing and winning rewards in the game. We are curious about whether this "underground economy" can be revived in an upright way in the Web3.

2 Play for FUN & Skill for EARN?

Certain games can actually help players develop some skills. For some high-level players, the game itself is an experience of continuous learning. Here we try to provide a new perspective. To some extent, the P2E business model can motivate individuals to actively seek the best solutions while improving skills. Some argue that Axie Infinity has reshaped jobs, partially replacing companies like Uber. Beyond gaming, Axie Infinity has a bold plan to reshape the economy and governance by showing what might be possible for people to work in Metaverse. In the white paper, Sky Mavis makes it clear that "you can think of Axie as a country with a real economy".

Simply speaking, games can be designed to reward skills, like League of Legends, or to reward hard work, like Clash of Clans. Abstractly speaking, what makes a game interesting in the long run is the gradually learning process (within a deep understanding of game mechanics). Imagine that many new-players and non-players systematically learn what Ethereum is, what DeFi is, what proof of stake (POS) is, and other Web3 concepts from playing the blockchain games.

CONCLUSION

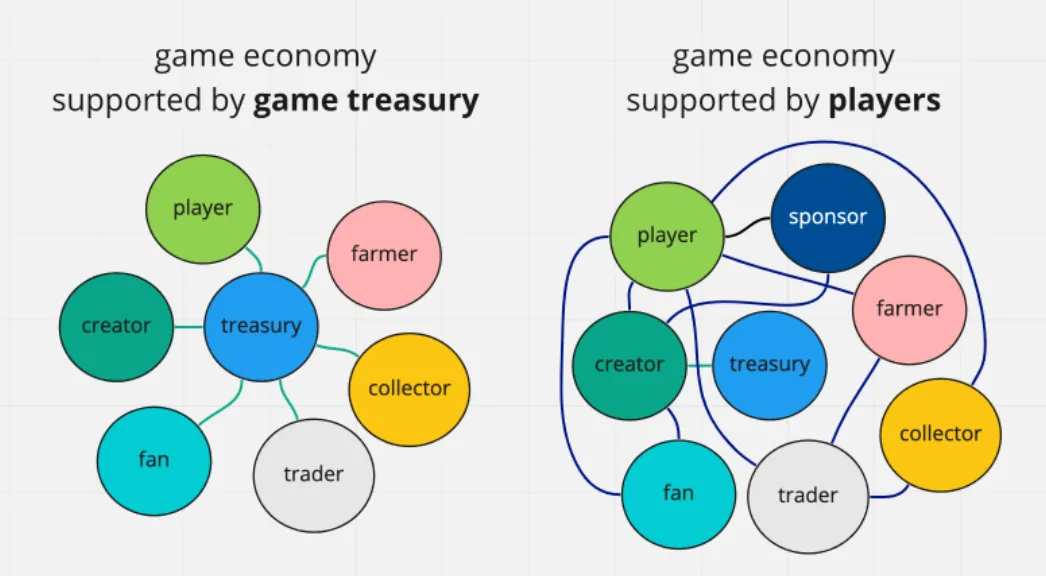

At present, both GameFi and Metaverse are in the early stage of development, we consider capturing opportunities from infrastructure and guild first. We are looking forward to the maturity of GameFi and other blockchain infrastructure, which will drive changes of content production and consumption in the gaming field. The future of GameFi should focus on building an ecosystem that allows players to create and directly exchange value, rather than game intermediaries earning profits. A vibrant economy should enable people to exchange goods and services with each other (see the chart at right).

After all, blockchain technology and NFT applications are only a tool to serve the game industry, how to use it depends on the co-creation of developers and consumers.

Works Cited

http://www.gamelook.com.cn/2022/06/486031

https://www.panewslab.com/zh/articledetails/1649295117423629.html

https://www.8btc.com/article/6728018

https://www.theblockbeats.info/tw/news/27691

https://0xcj.com/20220214306441.html

https://mirror.xyz/dunyi.eth/znadhdVe0t_z-9tSUB98CMyhxhGVcVF5SA4xUqr4uSQ

https://zombit.info/the-dilemma-and-way-out-of-blockchain-games/

https://mp.weixin.qq.com/s/adEI2RBfrVJMx9zD7kNQSQ

https://www.defidaonews.com/article/6733818

https://www.panewslab.com/zh/articledetails/1646875367712674.html

https://medium.com/borderless-capital/introduction-to-tokenomics-c7af75c09bfe

https://techflowpost.mirror.xyz/egpoVSqi1mC7Os2Qw1xFsp1MqDO_lnmYk6R4zHWG7d8?s=05

https://naavik.co/deep-dives/axie-infinity#axie-decon=

http://www.yuanli24.com/news/7226

https://mirror.xyz/dunyi.eth/znadhdVe0t_z-9tSUB98CMyhxhGVcVF5SA4xUqr4uSQ

https://cointelegraph.com/news/gamefi-is-showing-signs-of-a-mature-landscape-report

http://gamerboom.com/archives/45216

https://www.mytoken.io/news/79422.html

https://www.chaincatcher.com/article/2073194

https://www.theblock.co/post/36054/blockchain-gaming-part-iii-protocol-led-second-generation-games

https://www.okx.com/academy/en/play-to-earn-gamefi-explained#top-gamefi-projects

https://moralis.io/what-is-gamefi-and-play-to-earn-p2e/

https://zhuanlan.zhihu.com/p/521174798

https://www.blockvalue.com/news/20210928995304.html

https://messari.io/article/blockchains-changing-the-game

https://www.51cto.com/article/711596.html

https://www.blockglobe24.com/news02/76775.html

http://www.yuanli24.com/news/7226

https://www.blockvalue.com/news/20210928995304.html

https://www.blockvalue.com/p/80005.html

https://www.chaincatcher.com/article/2058051

https://www.8btc.com/article/6720498

https://www.newsbtc.com/all/blockchain-gaming-huntercoin/

https://naavik.co/deep-dives/axie-infinity#axie-decon=

https://www.tuoluo.cn/article/detail-14867.html

https://www.panewslab.com/zh/articledetails/1631860636388053.html

http://www.lianchaguan.com/archives/27963

https://zhuanlan.zhihu.com/p/485035825

https://zhuanlan.zhihu.com/p/521174798

https://zhuanlan.zhihu.com/p/381677572

https://www.zhihu.com/question/436567995

https://www.sohu.com/a/228222283_483399

https://www.blocktempo.com/about-ethereum-virtual-world-cryptovoxels/

https://blockcast.it/2022/01/18/challenges-gamefi-needs-to-solve-to-succeed/

https://messari.io/article/blockchains-changing-the-game

https://www.51cto.com/article/711596.html

https://www.btcfans.com/zh-cn/article/79361

http://www.gamelook.com.cn/2020/04/381260

http://www.gamelook.com.cn/2022/06/486031

https://www.newsbtc.com/all/blockchain-gaming-huntercoin/

https://www.blockvalue.com/news/20210928995304.html

https://crypto001.com/nft/11336.html

https://www.youxituoluo.com/525942.html

https://cowlevel.net/article/2093022

https://www.zhitongcaijing.com/content/detail/263657.html

https://www.defidaonews.com/article/6727334

https://www.theblockbeats.info/news/30815

http://www.gamelook.com.cn/2021/12/466515

Why Gamers Shouldn't Hate NFTs - by Ryan Sean Adams

Why Video Game Genres Fail: A Classificatory Analysis

5 Criteria to Take Into Account When Creating a Web3 Game | by Powder. gg | Medium