TL;DR

In this article we will take Venture DAOs as examples to discuss whether this market is worthy of joining in? We hope to figure out what factors benefit or damage Venture DAOs, and whether these problems can be solved in the future. Nowadays, in order to enter the cryptocurrency market, venture capital should target not only entrepreneurs, but also those in the investment world. We must increasingly participate in investment together with the overlapping roles of "community/investor/user". We believe that Venture DAOs will be a new venture capital paradigm worth practicing. We are more optimistic about two directions: small and precise quantitative Venture DAOs and broad, large Venture DAOs, which have the opportunities to integrate application layer resources to attain long-term value. So far, we cannot be optimistic enough to predict which of the many Venture DAOs will survive the test of time, and it may take more rounds of bull and bear market tests to screen out good projects that can really live through these cycles.

With crypto having boomed in 2021, there are now more than 180 DAOs managing over $10 billion in assets according to DeepDao, attracting nearly 2 million members. Just as the Limited Liability Company (LLC) has been the choice of organizational structure since the Industrial Revolution, the DAO portrays a new paradigm of human organization in Web3. The first part of this article we will briefly review the origin, definition, and core governance elements of a DAO. The second part we will take Venture DAOs as examples to discuss whether this market is worthy of joining in? We hope to figure out what factors benefit or damage Venture DAOs, and whether these problems can be resolved in the future.

1 Brief review: DAO Consensus and Formation Basis

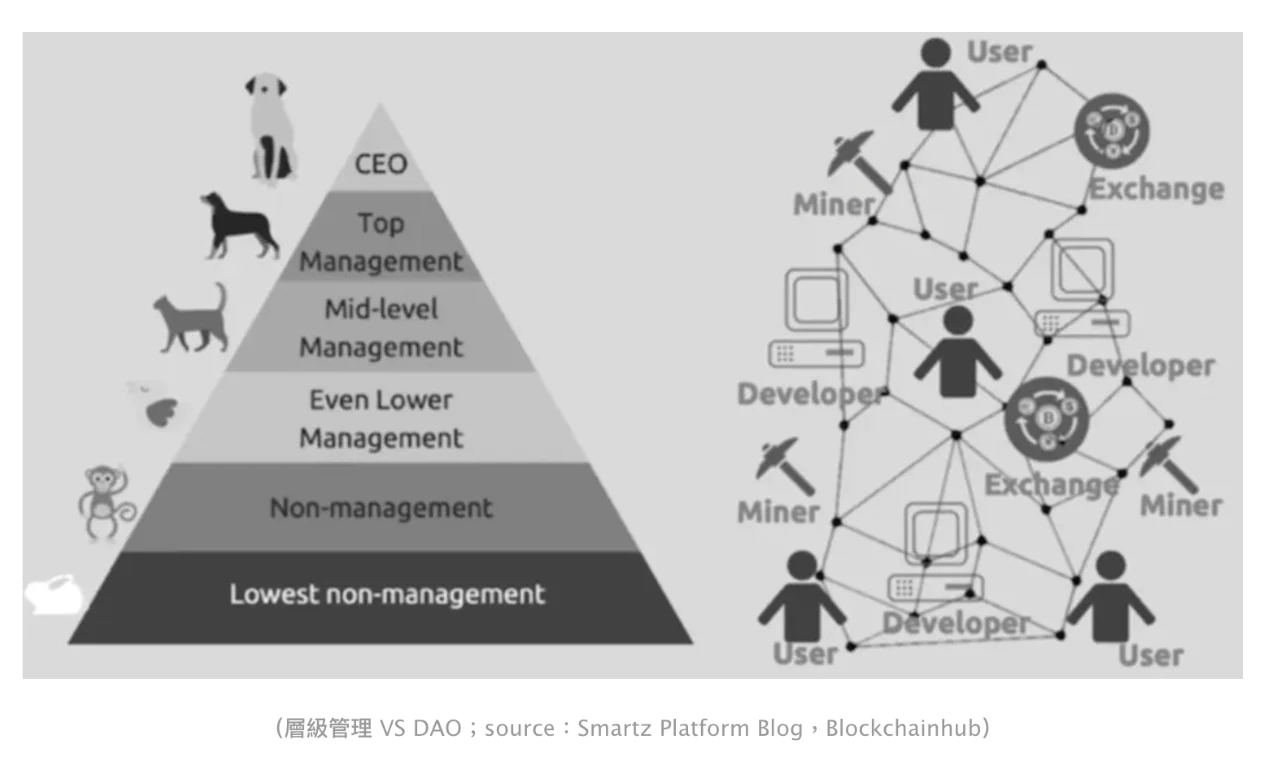

In 2014 Vitalik Buterin described DAO as a decentralized organization, “not a hierarchical structure managed by a group of humans and controlling property through a legal system, but involving a group of humans interact with each other according to a protocol specified in the code and executed on the blockchain.” Julia Rosenberg and Maria Gomez of Orca also tried to refine the definition of DAOs. They believe that DAOs are built on: 1) open sources and blockchains, 2) a public membership, 3) a group of independent parties, 4) using tokens to manage protocols, 5) the allocation of internal capital for the purpose of automated markets without collusion, and 6) incentives of bottom-up community engagement.

The origins of a DAO will not be expanded upon here. The primary distinction between DAOs and traditional organizations comes from its unique structure: The essence of a DAO should be an automated software protocol surrounded by a community.

From the above, we expect that DAOs can empower the production of different industries in various forms. The operation details of each DAO, whose type, structure, rules and governance depend on the participants and their goals. So far, we have seen three main use cases in the market: Protocol DAOs, Investment DAOs, and Social DAOs. Although these are currently in the stage of practical exploration, we believe that researching the path of the forerunners will help to clarify a blueprint for the future. Next, we will focus on Venture DAOs and discuss:

- How did Venture DAO arise?

We will review the organizational structure of the DAOs and the development trends of VC in the new era respectively. - How does a Venture DAO work? What difficulties exist or what problems might it bring up?

We will summarize how mainstream Venture DAOs capture market value in the field of investment, and then discuss about what problems exist and whether they can be completely solved in the long and short terms. -

Discuss whether the establishment of Venture DAOs is "the revolution of the old allocation rules" or "the definition of new allocation rules" - is a Venture DAO an evolutionary paradigm to replace the traditional VC structure, or does it provide a new possibility of organization structure?

- Analysis of the motivation of traditional venture capital institutions transforming into Venture DAOs: Can Venture DAOs meet the existing needs of the venture capital market? Can DAOs solve the shortcomings of traditional VC?

- What are the irreplaceable OR absolute advantages of Venture DAOs? Do Venture DAOs satisfy with the development trend of venture capital in the new era?

- How to define a successful Venture DAO in the future? Which application areas are we optimistic about?

We will discuss whether Venture DAOs are worth practicing in the above paragraphs, and then discuss in what aspects they might be successfully practiced to achieve sustainable development.

2 Will Venture DAO be the new paradigm in the new era of venture capital?

Before answering the necessity of the establishment of Venture DAOs, we try to review how traditional venture capital institutions meet market needs, as well as the current problems and possible trends for its future.

Venture capital (VC) firms are usually composed of a group of teams with professional knowledge and industry experience in diversified industries, for example technology, finance and capital operation, looking for startups with high growth opportunities. VCs provide startups with funds and resources in exchange for equity and ultimately bring them to the public market through an initial public offering (IPO), or they sell their investment and exit the company, often following mergers and acquisitions.

As early as 2017, a report by Pitchbook pointed out that due to the lack of long-term Limited Partnership (LP) in China, the average holding period of Chinese VC projects is only 3.3 years, compared with 8.2 years of that of the US. And in the US the identities of investors and entrepreneurs are often interchangeable. If VC institutions only focus on short-term profits and are oriented towards results with "low tolerance for failure", it will damage the incubation of a large number of basic research and innovation projects. Tian Xuan, a professor at Tsinghua PBC School of Finance, also pointed out that “it is necessary to have a higher tolerance for short-term failures of startup innovations." Under the current epidemic and the resulting difficulties in raising funds, the cost-effectiveness of venture capital merely pursuing short-term return incentives continues to decline. It means that the requirements for investment talent and the patience of investment cycles need to be further improved upon, and venture capitalists are increasingly in need of "entrepreneurial spirit".

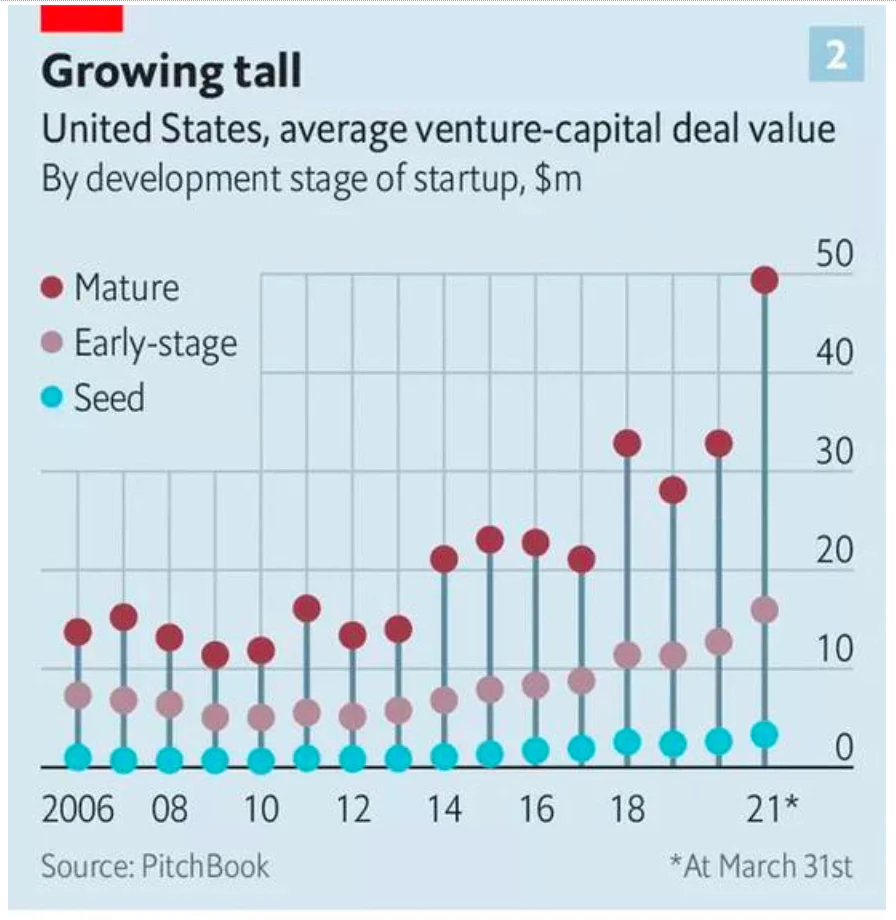

At the same time, the continued influx of venture capital has pushed up the average valuation of projects in the market, with many seed projects now being valued close to their Series A valuations a decade ago. The average seed-stage valuation of a U.S. startup in 2021 is $3.3 million, more than five times the 2010 level (The Economist, 2021). This also means that the extensive investment strategy of the old venture capital giants such as "investing the entire track" is unsustainable, thus refining more targeted investment strategies is necessary.

On the one hand, reshuffling and polarization of venture capital institutions increased. On the other hand, excellent projects are never short of money and their premiums are often too high in the current market situation. With the expansion of various groups participating in venture capital, the market competition has gradually intensified. Apart from VC firms, corporate venture capital departments are being established and challenging the existing concept of VC. Traditional venture capital institutions are also undergoing self-innovation, by seeking differentiation (focusing on investment and research in vertical tracks), expanding scale (increasing post-investment management and incubation services), and refining teams (such as sole proprietorship venture funds) and introducing innovative business models (venture capital accelerators).

Through the above review, we can see a trend that the “short-term and excess” returns that were once celebrated in the venture capital industry are gradually decreasing, and the boundaries between venture capital and other investment institutions are further blurring, for example some large VCs are more akin to asset management companies. The relationship between founders and venture capitalists may not be as important as it once was. Especially as startups grow, it may not matter who is investing, but how much you are willing to invest.

As a result, a new field of venture capital has been proposed, combining both DAOs and VCs. Some people hope that venture capital will no longer be the "power" of a few elites, and it will no longer be a game unique to well-connected venture capitalist institutions. Joyce Yang, founder of Global Coin Research, believes that "Global Coin Research's DAO goal is to subvert the traditional VC model, to democratize investment in the crypto-track, and to provide opportunities for those who have never invested before."

2.2 Venture DAOs - How does it work? What problems may arise, and can they be completely solved in the short and long term?

As early as 2016, The DAO on Ethereum can be regarded as the earliest form of Venture DAO. After 2018, MetaCartel, LAO, Flamingo DAO, Stacker Ventures, Angel DAO, Honey DAO, Komorebi Collective and many more appeared one after another. Most of the Venture DAO models are still based on building a treasury and decentralized management of how funds are invested, but there are differences in the entry thresholds and governance mechanisms of members. In addition, not all DAOs issue governance tokens. Some organizations with higher thresholds will combine on-chain governance with off-chain governance to promote the participation of community members, while some organizations with lower entry-thresholds involve token holders to be members in order to flourish the community.

In short, Venture DAO can be divided into two categories according to the degree of openness: public DAO and private DAO.

- Public DAO: Users can participate in the voting and governance of the community by holding tokens, and obtain the benefits of the project. Voting rights and income are related to the number of tokens held by the address. Retail investors and ordinary players can participate by purchasing tokens in the market, representing projects such as Whale and JennyDAO.

- Private DAO: Members need to be invited by other members to join the community. Most members of this type of DAO know the real identities of other members. The members gather together for a common belief or hobby (such as NFT), depicting what could be considered more of a high net worth player NFT "private club" for professionals. The community usually has its own native tokens, but most of them will not circulate in the secondary market and are only used within the community.

1 Can the “Wisdom of the Crowd” outperform the wisdom of a select few?

Investing is a highly professional activity, and high-return investment decisions are often counter-market consensus at the time of investment. At present, most of the Venture DAOs governance determines voting power by the number of tokens held, but that may easily lead to centralization of power among a certain group of tokenholders. Pursuing absolute democracy for individuals is not necessarily the optimal solution for decision-making. In addition to the "token stake" model, what better solutions might the market have in order to improve the above problems? The believability-weighted and radical transparency decision-making model derived from the Bridgewater Fund may provide a new perspective. Members are tagged with colleague and business partners’ comments, which might be permanently saved. We hope to see more Venture DAOs whose mechanisms allocate voting and member rights reasonably to preserve decision-making power.

2 How does the design mechanism of "proposal + voting" improve decision-making efficiency?

The trilemma in DAOs is "scale, quality, and access". In a small DAO, all members have enough energy to read all proposals and vote on them. "1 token = 1 vote" is enough. This supermajority principle with simple voting, quality and access can be maintained but is not scalable. To achieve both scale and quality, DAOs can employ more sophisticated vote weighting mechanisms, such as “ Holographic Consensus” or liquid democracy. This increases scalability while maintaining quality, but it is harder for voters to fully understand, which reduces accessibility and therefore legitimacy of decisions. They are also more difficult to implement, especially when voting takes place entirely on-chain.

Noticeably, there are hundreds of teams currently working on the above deficiencies, and DAO tools for governance, reporting, treasury management, and communication are thriving. In the short term, we feel that Venture DAOs governance is likely to remain chaotic. As the market matures, we believe truly effective DAO governance tools will show first.

3 Potential bribery and monopoly risks

These risks relate to the token distribution and voting right mechanisms associated with the tokens. As long as whales are large enough, they can manipulate proposals and votes by themselves or by conspiring with others, and thus monopolizing investment decisions . Whales can influence investment decisions by bribing guardians/voters, or launch a "Sybil attack" to pledge tokens in multiple wallets to vote, making DAO's investment decisions more in line with their own interests. The noise and disruption of DAO governance by short-term speculators is a test of the DAO's economic model design.

4 Technical Risks of Smart Contracts

At present, the DAO ecosystem is not perfect, and the possibility of hacking is a big risk. One of the largest crowdfunding projects, "TheDAO", lost a third of the 11.5 million ETH it raised due to the hack, losing nearly $60 million.If this happens, the absence of investor protection systems could lead to huge losses for individual investors.

5 Limited investment credit and investment scope?

Although investing in DAO can to a certain extent avoid the selling pressure of large institutions after the launch of investment projects, and the investment amount is relatively smaller than that of large institutions, the lack of endorsement by large institutions and the uncertainty of early projects are also worth considering. Excellent projects/entrepreneurs can usually find excellent venture capital. CultDAO has a very controversial ideology, which may discourage many excellent projects. If there is no high return on investment to turn the positive flywheel, only selling its ideology might lead to a “meme” VC DAO.

6 Risks to Legal Tax System Compliance

DAOs also need to overcome many potential regulatory and legal challenges. Whether the DAO can be accepted by the government as a qualified “investment subject” deserves flexibility, and whether a partner who is not regarded as a “corporate body” can become the subject of property registration is still a question; how will the investment be submitted for tax filing after income is obtained? Jeremy Coffey, a nonprofit expert at the Perlman law firm, said the new structure of the Venture DAO could lead to a range of issues, from jurisdictional oversight and tax issues to securities law. Regulatory uncertainty makes it difficult for DAOs to interact with brick-and-mortar companies, which is a headwind. While the U.S. state of Wyoming pushed for legislation that would allow DAOs to operate on the same legal basis as traditional LLCs, while allowing them to be governed by their own smart contracts, this was met with resistance from the U.S. Securities and Exchange Commission (SEC). While we've seen a16z have some good advice on how to create a legitimate DAO entity as an unincorporated non-profit association, the standardization of DAO investments for the foreseeable future and improving their compatibility with existing legal/tax systems is critical.

7 Potential zero risk of issuing coins

An important element in DAO is the governance token. Token holders have the power to shape the future of the DAO, and they can influence decisions related to the projects, such as changing how the funds are used. Owning a governance token is a bit like taking an equity stake in the early days of a startup – if it succeeds in the future, the stake will be very valuable. But the risk is that these governance tokens might turn into zero value. Investors should do their homework and assess the losses they can afford before joining in. At the same time, Venture DAOs that choose to issue tokens also need to face compliance and regulatory issues.

We see that in terms of organizational structure, DAO-driven VC can indeed be described as a new organizational production model in the venture capital industry. At present, it mainly relies on the power of initiating KOLs and organizations to establish its own governance framework, incentive mechanism, project incubation and consensus culture. That is, a hybrid model of "on-chain + off-chain" governance. Most of them limit the issuance of tokens, or strip the rights and interests of the community and governance, or raise the entry threshold for members. But the unavoidable problem is that many DAOs will encounter resource dissipation problems in the process of development, such as deviation from the original intention, communication disputes and disputes in different cultural backgrounds. Especially in the early stage of DAO, it still needs a relatively centralized organization to promote it to be effective.

2.3 Is Venture DAO an evolutionary paradigm to replace the traditional VC structure, or a new structure of organizations?

From a dialectical point of view, why should traditional venture capital institutions have motivations to transform into Venture DAOs? Can the DAO meet the market needs and solve the problems under the existing structure, or meet the development trend in the new era of venture capital? We believe the answer is the latter, and the DAO provides more possibilities for VCs to operate in the future.

We have mentioned earlier that the “short-term and excess” returns of the venture capital market gradually declined, which means that the market requirements for making decisions should be more precise and time-sensitive. We doubt that the paradigm of Venture DAO can improve alpha returns better than the GP-LP system. Also, it might not improve decision-making efficiency in the way of Venture DAOs. Correct investment decisions are often anti-consensus at the beginning, and decision-makers should be elitist enough and have their own alpha capture strategies, which do not require democratic voting.

From the perspectives of “fundraising” and “selecting”, as the market liquidity gets better, startups can reach mutual investors in a more direct and fair way. Based on the decentralized mechanism, projects with sufficient fundraising can reduce the operation costs of intermediaries, and have competitive advantages against the platform effects and private networks.

Will future investment institutions necessarily “know the project better than the project owner”? Let us discuss it from a different perspective. For the crypto market, many blockchain projects from cornerstone investment, to private equity (equity investment + Token), and then to exchanges for initial coin offering (ICO), are particularly fast.

From this, we try to answer a key question: Must Venture DAOs issue tokens for governance? Our answer is YES. How Venture DAOs decide to hold or trade tokens that are already in the public market is different from the long-term holding of traditional VC funds. For a long time, large-scale venture capital institutions or investors have bought at a relatively low price in the early rounds and exited for profits after the project was launched. In many cases at present, projects in the crypto market have already been listed on chain after they have completed a round of financing with investors, and even no need of raising from VCs. There is no concept of Series ABCDE or Pre-IPOs as before. The barriers between "primary market" and "secondary market" in traditional cognition have been greatly weakened. As a venture capital fund, if it does not invest in the previous rounds, it is highly likely that it needs to openly trade with retail investors on the exchange.

It is worth mentioning that the ready-to-exit/enter funding model also brings more possibilities to the crypto market. Venture DAOs are able to capture a continuous funding to avoid the sell-off phenomenon of traditional VCs to a certain extent. This model may be more suitable for investing in infrastructure with high technical barriers. The short-term alpha might not be particularly obvious, however in the long-term cycle, it can capture the beta benefits of the market by building influence at the protocol layers and application layers.

In a word, Venture DAOs will not be a process to replace the traditional VC structure, but provide a new way of production organization structure. In the short term, operating investment DAO is just a model difference, trying to establish the influence of "media and communication" in the field of Web3 still relies on initial resources. The existing projects in the market have to be tested through multiple rounds of bear markets before we can conclude clearer criteria of judging the pros and cons.

2.4 How will the future Venture DAO be like in order to achieve sustainable development? Which application areas of Venture DAOs are we optimistic about?

"What is being reorganized? What needs to be decentralized?" The open source and decentralized nature of blockchain redefines the relationship between protocols and investors. Theoretically, it allows everyone in the world to come together and create a VC. We discussed in the first three sections that Venture DAOs might be a viable investment experiment. In this part, we will discuss its promising application fields.

One voice is that the Venture DAOs should be sufficiently "small and sophisticated". In a sufficiently liquid market, there should be no distinction between primary and secondary market. A Web3-native Venture DAOs can use DeFi projects to raise funds and tokenize the cash flow. All economic activities and rules based on DAOs are recorded on the blockchain, the assets invested by it are digital and traceable on-chain assets, and its investment performance is verifiable. This type of index-based Venture DAO, such as index coop, is an automatic trust mechanism based on simple (even complex) transactions, building direct indicators (economic value) to measure the benefits of decisions. In contrast, traditional venture capital without quantifiable attributes may be more uncertain.

Another voice is that a sufficiently large Venture DAOs may be an opportunity to integrate infrastructure protocols. The innovation of the infinite fundraising model may not be something that a small-scale, short-term organization can do, since its short-term alpha will not be particularly obvious. It is necessary to capture longer-term value at the application layers based on infrastructure protocols.

CONCLUSION

"What happens when you reduce the cost of setting up an investment fund by a factor of 1000?" The answer is that setting up an investment fund is as easy as tweeting - we don't recommend setting up an investment fund by tweeting. But when it's that simple, the world looks completely different because creativity is absolutely phenomenal. ”——Will Papper, Co-founder of Syndicate Protocol.

We believe that Venture DAO will be a new venture capital paradigm worth practicing. Now to enter the cryptocurrency circle, venture capital should target not only entrepreneurs, but also those in the investment world. "Peers" are not just other venture capitalists. They must increasingly participate in investment together with the overlapping roles of "community/investor/user". We are more optimistic about two directions: small and precise quantitative Venture DAOs and broad, large Venture DAOs, which have the opportunities to integrate application layer resources to attain long-term value. So far, we cannot be optimistic enough to predict which of the many Venture DAOs will survive the test of time, and it may take more rounds of bull and bear market tests to screen out good projects that can really live through these cycles.

No matter what form of DAO, its biggest advantage may also be its biggest flaw: an ideal system design that can cooperate seamlessly without "trust" requires a group of "like-minded" partners to work together in the same original aspiration, gathered together under the guidance of the realization. If the advanced form of an ideal institution discards a key part of our human nature, then we have reason to maintain the necessary attention and vigilance against it. Only the production relations that adapt to the productive forces can promote the sound development of the economy and society. Perhaps the greatest value and significance of DAO is to establish a production relationship for us to meet the development needs of the new era, and to provide an appropriate social experiment. Tracheopteryx, a core contributor to Yearn Finance, said, “If you look at DeFi, it’s a bet on the future of finance; NFTs could be a bet on art, real estate, or any type of property. But DAOs are a bet on the future of how humans organize, which is a much bigger thing.” Thus, we need the pioneers of Venture DAO, and we need to keep studying them.